Situation

Beth (62) has diligently saved for retirement and has accumulated $3,545,220 in her traditional IRA and 401(k). Being only a few years away from retirement, she has been speaking with her financial advisor about what to expect and how to protect her retirement savings.

One of the things that her financial advisor discussed with her is the traditional IRA and

401(k) will be taxed at 35% when distributed. She finds out that by the time the traditional IRA and 401(k) are at zero, she will have paid $1,240,827 in taxes.

Beth’s financial advisor has recently started implementing a retirement tax mitigation strategy. This strategy can reduce or eliminate distribution taxes owed on a traditional IRA and 401(k). Plus, it has the added benefit of creating a post-retirement income stream.

Solution

Beth and her financial advisor discuss the ARP strategy in detail. The key component of this strategy is the creation of an LLC, which Beth will work for. The LLC will then create a 401(k), into which Beth will roll her traditional IRA and 401(k). This 401(k) will make annual distributions into a specialized insurance product of $709,044 for five years. After five years, the 401(k) will be at zero and the specialized insurance product will be distributed to Beth.

Beth plans to keep the principal in a specialized insurance product, creating an annual distribution of $248, 165 and creating a revenue stream for Beth to use during her retirement. This specialized insurance product maintains the tax characteristics of a Roth IRA, including tax-free gains and distributions. The specialized insurance product mitigates risk in investments, offers the potential to earn on interest rate arbitrage, and guarantees no loss of the principal balance. The specialized insurance product also provides a death benefit independent of the cash balance.

Result

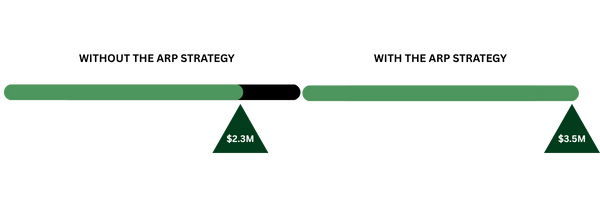

Beth would have a 35% tax rate on distributions with the traditional IRA and 401(K). With a retirement savings balance of $3,545,220, Beth’s tax obligation on the total distribution of $3,545,220 would amount to $1,240,827.

By implementing the ARP strategy, Beth can reduce or even eliminate the taxes on her qualified plan distributions. The strategy would annually distribute $709,044 to the specialized insurance product from her traditional IRA and 401(k) for five years. The specialized insurance product will invest the principal, generating $248,165 in distributions annually. Since Beth can use the principal in the plan as collateral on a loan, she will never have to remove any principal form the strategy. By implementing the ARP strategy, Beth achieves a tax savings of $1,240,827 and created an income stream of $248,165 annually, providing her with financial security in her retirement.